Payday Loans

Get a Free Savings Quote* & Consultation

Financial education and referrals—so you can choose with confidence.

Payday Loans (Education & Referrals)

If payday or cash-advance loans are stacking up—or you’re borrowing to cover prior fees—you’re not alone. Money Student is a financial education and referral platform. We can help you understand your options and, if you choose, introduce you to independent providers who may be able to assist.

What is a payday (cash-advance) loan?

A payday loan is a short-term, small-dollar loan typically due on your next payday. Lenders charge a flat fee rather than a traditional APR, but that fee often translates into a very high effective APR. Many borrowers repay by giving the lender permission to debit a bank account or by providing a post-dated check.

Example: Borrow $500 and pay a $75 fee for two weeks. You’ll owe $575 at repayment. If you can’t pay and “roll over” the loan for another two weeks, you’ll likely pay another fee, and the costs add up quickly.

Why these loans are hard to escape

-

-

- Lump-sum repayment due on your next payday can crowd out rent, utilities, or groceries.

- Rollovers and repeat borrowing increase total fees without reducing the principal.

- Multiple concurrent loans (online + storefront) can make tracking due dates and bank debits difficult.

-

Options that may help

Depending on your situation, one or more of these paths may be worth exploring:

-

-

- Payment plans with your lender. Some lenders may offer extended repayment plans once requested.

- Debt management (credit counseling). A nonprofit credit counselor may help create a budget and a structured plan for certain eligible debts.

- Debt resolution/settlement (unsecured debts). For qualified accounts in hardship, a third-party company may attempt to negotiate reduced payoff amounts.

- Personal loan consolidation. If approved, replacing multiple high-fee advances with a fixed-rate installment loan could lower total costs and simplify payments.

- Hardship assistance & budgeting support. Temporary expense cuts, payment deferrals on other bills, or local assistance programs may create room to exit the cycle.

-

We’re happy to walk through pros and cons of each option and, if you want help, refer you to an independent provider that fits your goals and budget.

What to watch for

-

-

- Repeat rollovers and add-on fees.

- Multiple debits hitting your bank account on the same day.

- New loans to pay old loans (often a sign the plan isn’t sustainable).

- State rules. Availability, fees, and caps vary by state; some states restrict or prohibit certain payday products.

-

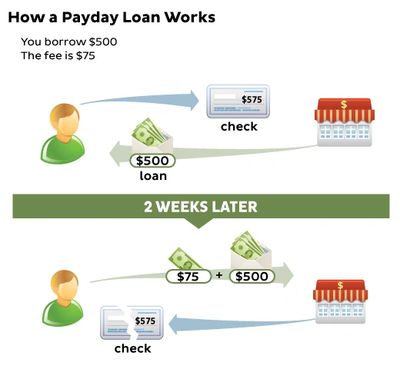

Example of Payday Loan Fees

- You borrow $500. The fee is $75.

- You give the lender a check for $575.

- The lender keeps your check and gives you $500 in cash.

- After two weeks, you give the lender $575 cash, and you get your check back.

- The bottom line: You paid $75 to borrow $500 for two weeks.

What happens if I can’t pay the lender the money I owe?

If you cannot pay the lender the money you owe, you borrow the money for two more weeks. This is called a “rollover,” or “rolling over” the loan. To rollover the loan, you pay another fee. These high fees add up quickly and make it extremely hard to pay off the principal balance.